Off Balance Sheet funding of receivables from small and medium size buyers

Identifying investors who would invests in the receivables in a commercially viable manner

Structure to be replicable and scalable so that it can be expanded.

Considering the short tenor of the receivables, any solution would need to allow for reusing the reporting, collection and receivables management infrastructure that will be created to cater to the monitoring and credit compliance requirements of investors

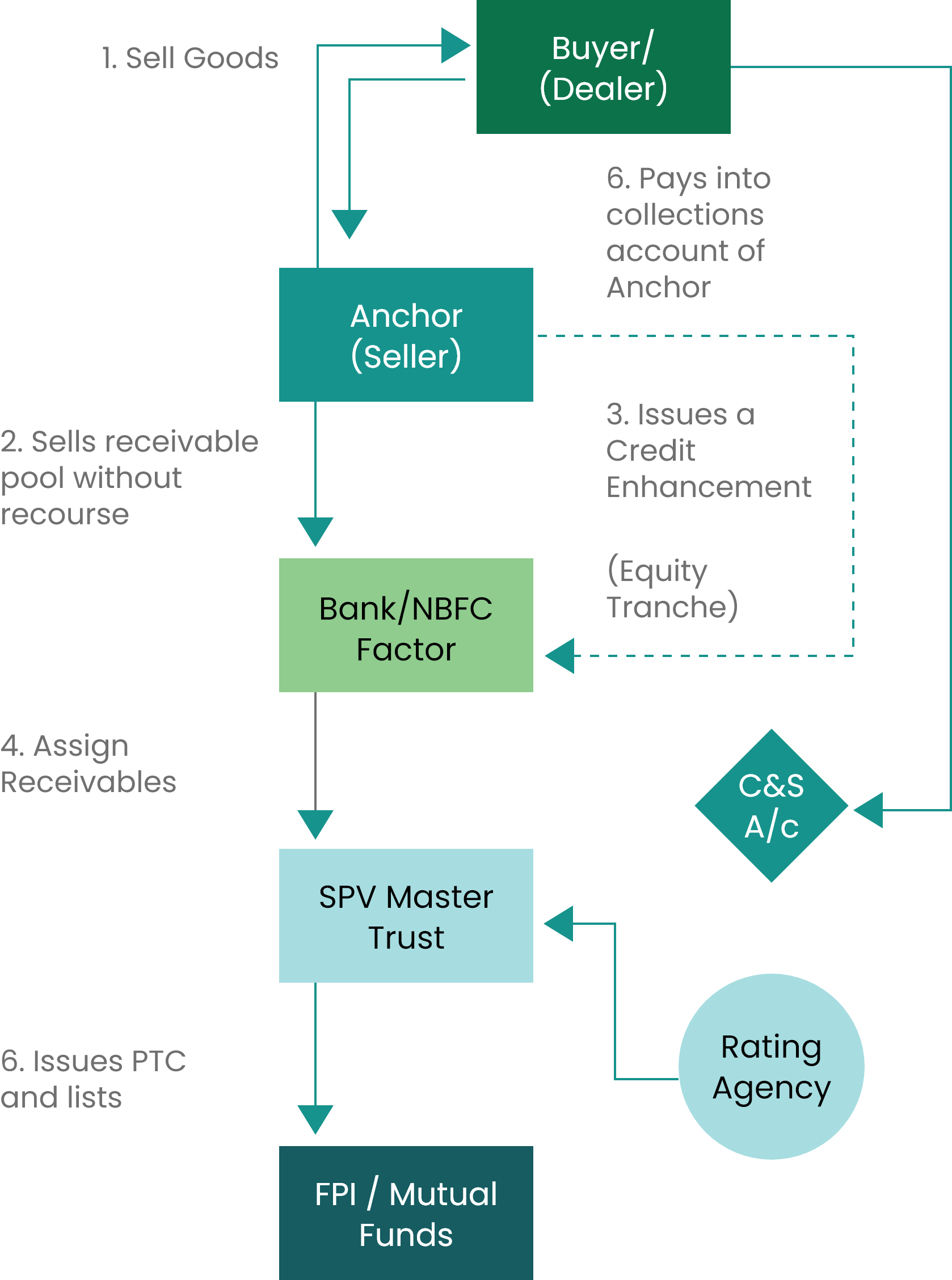

Seller/Anchor sells goods to dealers/buyers and once invoices are accepted , the receivables are created on sellers' books.

Agreement between Bank and seller should confirm that a buyer/dealer confirmation removes the risk of disputes or set off. And receivables are then sold to the bank

The Bank settles a SPV trust and assigns the above receivables to the SPV which in turn issues a Pass Through Certificate(PTC)

Pass Through Certificate – an instrument signifying beneficial ownership in the underlying assets held in the trust managed by Trustee and rated by an approved rating agency

The PTC would be sold to Investor(s). The Trustee is holding the receivables on behalf of the Investors and is the legal owner.

The PTC are transferable and issued in lot sizes. They are usually de-materialized and credited to the Demat account of the investor.

Dealer pool which qualifies for priority sector lending to be preferred, for maximum bank participation

Veefin Capital Private Limited is a Reserve Bank of India–registered Non-Banking Financial Company (NBFC). We are a non-deposit taking entity focused on providing compliant, technology-driven financing solutions to MSMEs and businesses across India.

Copyright © . Veefin Capital Ltd.